Marginal cost refers to the additional expense incurred from producing one more unit of a good or service, while marginal benefit represents the extra gain received from that additional unit. Efficient economic decisions occur when marginal benefit equals marginal cost, ensuring resources are allocated optimally. Understanding this balance helps businesses maximize profits and consumers optimize satisfaction.

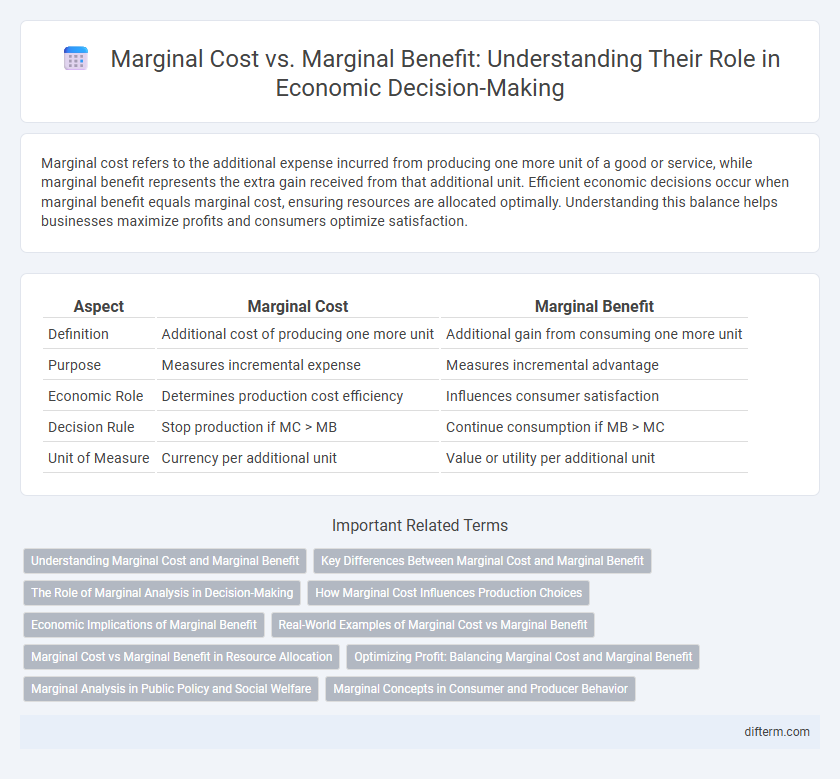

Table of Comparison

| Aspect | Marginal Cost | Marginal Benefit |

|---|---|---|

| Definition | Additional cost of producing one more unit | Additional gain from consuming one more unit |

| Purpose | Measures incremental expense | Measures incremental advantage |

| Economic Role | Determines production cost efficiency | Influences consumer satisfaction |

| Decision Rule | Stop production if MC > MB | Continue consumption if MB > MC |

| Unit of Measure | Currency per additional unit | Value or utility per additional unit |

Understanding Marginal Cost and Marginal Benefit

Marginal cost represents the additional expense incurred from producing one more unit of a good or service, while marginal benefit refers to the extra satisfaction or value gained from consuming that additional unit. Understanding these concepts helps businesses and consumers make informed decisions by comparing the incremental costs and benefits to maximize net gain. Efficient allocation of resources occurs when marginal cost equals marginal benefit, marking the optimal point of production and consumption.

Key Differences Between Marginal Cost and Marginal Benefit

Marginal cost represents the additional expense incurred from producing one more unit of a good or service, directly impacting a firm's production decisions. Marginal benefit measures the extra satisfaction or revenue gained from consuming or producing an additional unit, guiding consumer choices and market equilibrium. The key difference lies in marginal cost being a supply-side consideration, while marginal benefit reflects demand-side value assessment.

The Role of Marginal Analysis in Decision-Making

Marginal analysis plays a crucial role in decision-making by comparing marginal cost and marginal benefit to optimize resource allocation and maximize profit. When the marginal benefit exceeds the marginal cost, businesses and individuals increase production or consumption, whereas decisions are reversed when marginal cost surpasses marginal benefit. This economic principle ensures efficient utilization of scarce resources, guiding choices in production levels, pricing, and consumption to achieve equilibrium.

How Marginal Cost Influences Production Choices

Marginal cost directly impacts production decisions by determining the expense of producing one additional unit of output. Businesses increase output only when the marginal benefit, or additional revenue, exceeds the marginal cost, ensuring profitability. Efficient allocation of resources occurs when marginal cost aligns with marginal benefit, optimizing overall economic welfare.

Economic Implications of Marginal Benefit

Marginal benefit represents the additional satisfaction or utility gained from consuming one more unit of a good or service, guiding optimal consumer decisions in resource allocation. In economic terms, when marginal benefit exceeds marginal cost, it signals a profitable opportunity for production and consumption, increasing overall welfare. Understanding marginal benefit helps businesses and policymakers evaluate the efficiency of resource distribution and maximize economic growth.

Real-World Examples of Marginal Cost vs Marginal Benefit

Marginal cost refers to the additional expense incurred from producing one more unit of a good or service, while marginal benefit is the added satisfaction or utility gained from consuming that unit. For example, a factory deciding to produce one extra car weighs the marginal cost of materials and labor against the marginal benefit of the selling price and customer demand. In consumer behavior, a shopper considers the marginal benefit of purchasing an additional item against the marginal cost in terms of price and budget constraints, illustrating how these concepts drive economic decision-making.

Marginal Cost vs Marginal Benefit in Resource Allocation

Marginal cost represents the additional expense incurred from producing one more unit of a good or service, while marginal benefit measures the added satisfaction or utility gained from that unit. Efficient resource allocation occurs when marginal cost equals marginal benefit, ensuring that resources are neither underused nor overextended. Deviations from this equilibrium lead to inefficiencies, causing either wasted resources or missed opportunities for maximizing economic welfare.

Optimizing Profit: Balancing Marginal Cost and Marginal Benefit

Optimizing profit requires balancing marginal cost, the expense of producing one additional unit, with marginal benefit, the revenue generated from that unit. Firms maximize profit when marginal cost equals marginal benefit, ensuring resources are allocated efficiently without overspending. Understanding this equilibrium helps businesses make informed production decisions and achieve sustainable economic growth.

Marginal Analysis in Public Policy and Social Welfare

Marginal analysis in public policy evaluates the additional benefits and costs of social welfare programs to optimize resource allocation and improve societal outcomes. Policymakers assess the marginal cost of expanding services against the marginal benefit to determine the most efficient level of intervention that maximizes social welfare. This approach ensures that government spending achieves the greatest incremental improvement in public well-being while minimizing wasteful expenditure.

Marginal Concepts in Consumer and Producer Behavior

Marginal cost represents the additional expense incurred by producing one more unit of a good, directly impacting producer decisions and supply levels. Marginal benefit reflects the extra satisfaction or utility a consumer gains from consuming one additional unit, influencing demand and purchase choices. The equilibrium in markets is achieved when marginal cost equals marginal benefit, guiding optimal production and consumption behaviors.

Marginal cost vs Marginal benefit Infographic