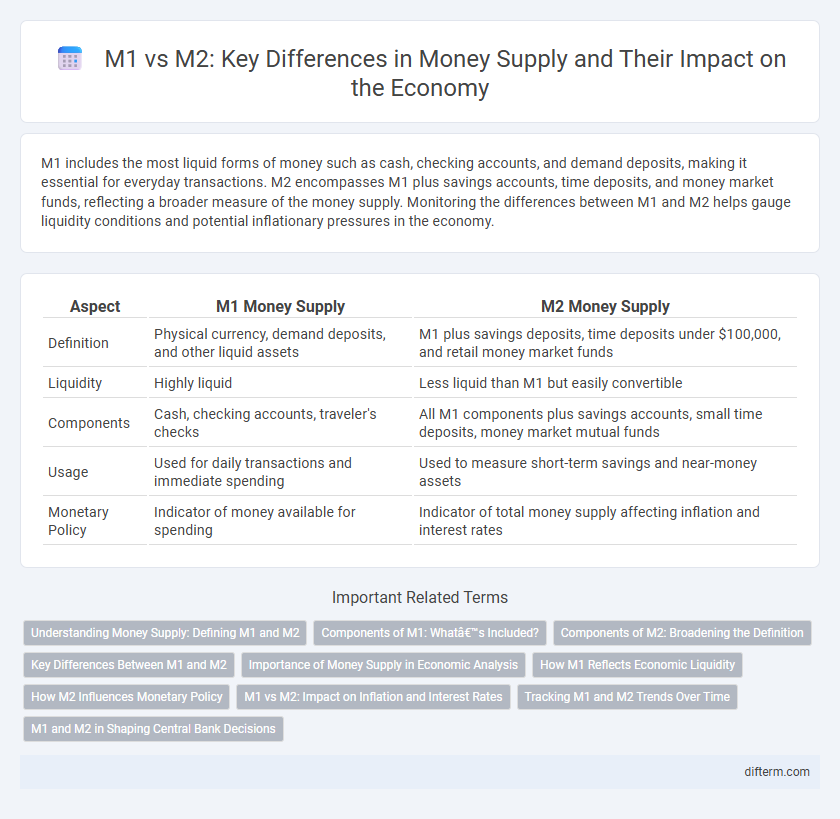

M1 includes the most liquid forms of money such as cash, checking accounts, and demand deposits, making it essential for everyday transactions. M2 encompasses M1 plus savings accounts, time deposits, and money market funds, reflecting a broader measure of the money supply. Monitoring the differences between M1 and M2 helps gauge liquidity conditions and potential inflationary pressures in the economy.

Table of Comparison

| Aspect | M1 Money Supply | M2 Money Supply |

|---|---|---|

| Definition | Physical currency, demand deposits, and other liquid assets | M1 plus savings deposits, time deposits under $100,000, and retail money market funds |

| Liquidity | Highly liquid | Less liquid than M1 but easily convertible |

| Components | Cash, checking accounts, traveler's checks | All M1 components plus savings accounts, small time deposits, money market mutual funds |

| Usage | Used for daily transactions and immediate spending | Used to measure short-term savings and near-money assets |

| Monetary Policy | Indicator of money available for spending | Indicator of total money supply affecting inflation and interest rates |

Understanding Money Supply: Defining M1 and M2

M1 represents the most liquid forms of money, including physical currency, demand deposits, and other checkable accounts, facilitating everyday transactions. M2 encompasses M1 plus near-money assets such as savings deposits, small-denomination time deposits, and retail money market mutual funds, indicating a broader measure of money supply impacting economic activity. Understanding the distinction between M1 and M2 is essential for analyzing monetary policy effects, inflation trends, and liquidity in the economy.

Components of M1: What’s Included?

M1 money supply primarily consists of the most liquid forms of money, including physical currency such as coins and paper money held by the public, demand deposits like checking accounts, and traveler's checks. These components are readily accessible for daily transactions and are critical indicators of economic activity and liquidity in the financial system. Unlike M2, which includes broader savings instruments, M1 focuses strictly on money that can be quickly used for spending.

Components of M2: Broadening the Definition

M2 expands upon M1 by including not only physical currency and demand deposits but also savings deposits, time deposits under $100,000, and retail money market mutual fund balances. This broader definition captures a wider array of liquid assets that households and businesses can access quickly, reflecting overall money supply more comprehensively. Understanding M2's components provides insight into consumer liquidity and potential spending power beyond immediate cash and checking accounts.

Key Differences Between M1 and M2

M1 includes the most liquid forms of money such as physical currency, demand deposits, and checkable deposits, making it essential for daily transactions. M2 encompasses all of M1 plus near-money assets like savings accounts, money market funds, and certificates of deposit under $100,000, representing a broader measure of the money supply. The main difference lies in liquidity, with M1 being readily accessible for spending while M2 provides insight into overall money availability and potential spending power in the economy.

Importance of Money Supply in Economic Analysis

M1 and M2 are critical indicators of money supply that influence economic analysis and policymaking. M1 includes highly liquid assets such as cash and checking deposits, directly impacting consumer spending and demand. M2 encompasses M1 plus savings deposits and time deposits, providing a broader view of money availability that affects inflation, interest rates, and overall economic growth.

How M1 Reflects Economic Liquidity

M1 money supply, consisting primarily of physical currency and demand deposits, directly reflects economic liquidity by measuring the most accessible forms of money available for immediate spending. Unlike M2, which includes savings accounts and time deposits that are less liquid, M1 captures the instantaneous purchasing power circulating within the economy. Tracking changes in M1 helps analysts gauge short-term economic activity and the ease with which consumers and businesses can conduct transactions.

How M2 Influences Monetary Policy

M2, which includes M1 plus savings deposits, time deposits, and other near-money assets, provides a broader measure of money supply that central banks monitor to assess liquidity conditions. Changes in M2 influence monetary policy decisions by signaling shifts in consumer spending and investment behavior, guiding interest rate adjustments and open market operations. Policymakers rely on M2 trends to gauge inflationary pressures and economic growth potential, shaping strategies to maintain price stability and support employment.

M1 vs M2: Impact on Inflation and Interest Rates

M1 money supply, consisting of physical currency and demand deposits, directly influences short-term liquidity and consumer spending, often leading to immediate effects on inflation and interest rates. M2, which includes M1 plus savings deposits and time deposits, reflects broader money availability, impacting medium to long-term inflation trends and monetary policy decisions. Central banks monitor the growth rates of M1 and M2 to gauge inflationary pressures and adjust interest rates accordingly to maintain economic stability.

Tracking M1 and M2 Trends Over Time

Tracking M1 and M2 trends over time reveals critical insights into liquidity and economic activity, with M1 encompassing physical currency and checking deposits, while M2 includes M1 plus savings accounts and time deposits. Changes in M1 often indicate shifts in immediate spending power, whereas M2 fluctuations reflect broader monetary availability affecting inflation and growth. Analyzing historical data from sources like the Federal Reserve provides a nuanced understanding of monetary policy impacts and economic cycles.

M1 and M2 in Shaping Central Bank Decisions

M1, consisting of physical currency and demand deposits, provides central banks with immediate insights into liquidity and spending behaviors, critical for monetary policy decisions. M2 expands this view by including savings deposits, time deposits, and other near-money assets, offering a broader perspective on overall money supply and economic activity. Central banks analyze shifts between M1 and M2 to calibrate interest rates, control inflation, and support economic growth effectively.

M1 vs M2 (money supply) Infographic