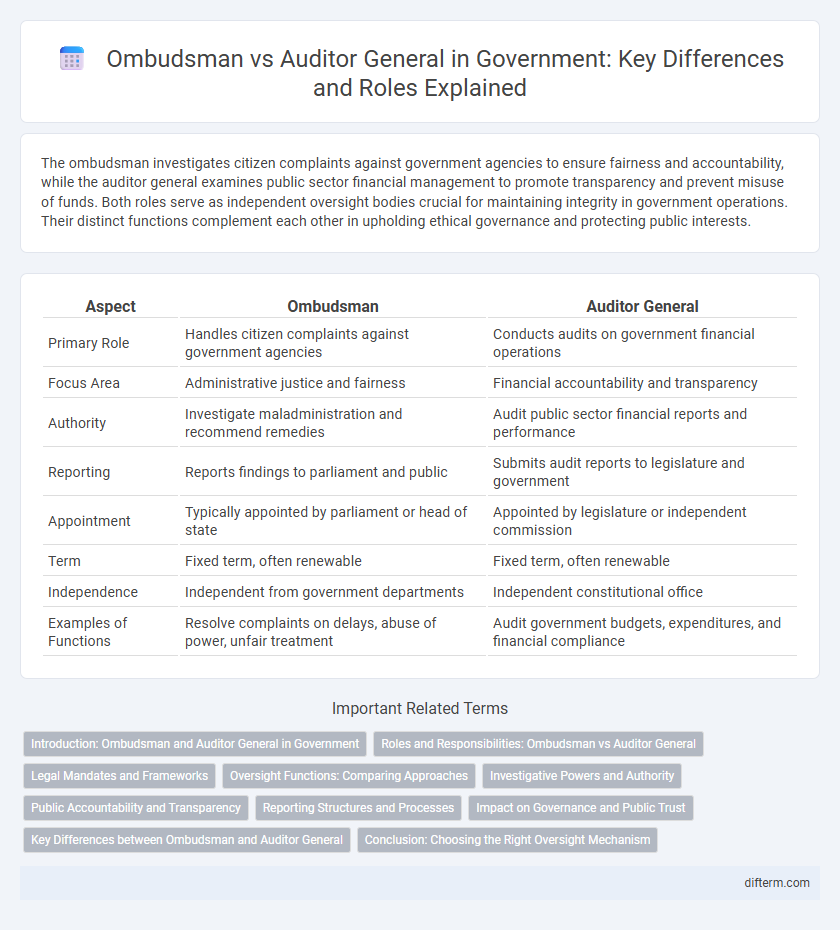

The ombudsman investigates citizen complaints against government agencies to ensure fairness and accountability, while the auditor general examines public sector financial management to promote transparency and prevent misuse of funds. Both roles serve as independent oversight bodies crucial for maintaining integrity in government operations. Their distinct functions complement each other in upholding ethical governance and protecting public interests.

Table of Comparison

| Aspect | Ombudsman | Auditor General |

|---|---|---|

| Primary Role | Handles citizen complaints against government agencies | Conducts audits on government financial operations |

| Focus Area | Administrative justice and fairness | Financial accountability and transparency |

| Authority | Investigate maladministration and recommend remedies | Audit public sector financial reports and performance |

| Reporting | Reports findings to parliament and public | Submits audit reports to legislature and government |

| Appointment | Typically appointed by parliament or head of state | Appointed by legislature or independent commission |

| Term | Fixed term, often renewable | Fixed term, often renewable |

| Independence | Independent from government departments | Independent constitutional office |

| Examples of Functions | Resolve complaints on delays, abuse of power, unfair treatment | Audit government budgets, expenditures, and financial compliance |

Introduction: Ombudsman and Auditor General in Government

Ombudsman and Auditor General are essential oversight institutions in government, ensuring transparency and accountability. The Ombudsman addresses citizen complaints regarding administrative injustices, promoting fair public service. The Auditor General conducts independent audits of government financial operations, safeguarding public funds against mismanagement.

Roles and Responsibilities: Ombudsman vs Auditor General

The Ombudsman addresses citizens' complaints against government maladministration, ensuring fairness and accountability through independent investigations and dispute resolution. The Auditor General conducts financial audits of government departments, assessing the accuracy of public accounts and compliance with laws to promote transparency and fiscal responsibility. Both offices serve as vital oversight mechanisms but focus respectively on administrative justice and financial integrity within government operations.

Legal Mandates and Frameworks

The Ombudsman operates under a legal mandate to address public complaints related to maladministration and protect citizens' rights within government agencies, often established by specific ombudsman acts or statutes. The Auditor General is legally mandated to audit government financial operations and ensure transparency, accountability, and the lawful use of public funds, guided by public audit laws and financial regulations. Both entities function within distinct legal frameworks designed to enforce oversight, with the Ombudsman focusing on administrative justice and the Auditor General on financial integrity.

Oversight Functions: Comparing Approaches

The Ombudsman primarily focuses on investigating complaints from citizens about maladministration and ensuring government accountability through dispute resolution and recommendations, while the Auditor General conducts systematic audits of government finances and operations to assess compliance, efficiency, and effectiveness. The Ombudsman uses a case-by-case approach to oversee administrative justice, whereas the Auditor General employs a broad, data-driven method to detect financial irregularities and performance issues across government agencies. Both institutions enhance public sector transparency but apply distinct oversight mechanisms tailored to legal compliance and administrative fairness.

Investigative Powers and Authority

The Ombudsman holds the authority to investigate complaints related to maladministration and abuse of power in government agencies, focusing on individual grievances and ensuring administrative accountability. The Auditor General possesses broad investigative powers to examine government financial records and audit public expenditures, aiming to promote transparency and prevent fiscal mismanagement. Both entities operate independently but serve complementary roles in overseeing government operations through distinct domains of investigative authority.

Public Accountability and Transparency

The Ombudsman ensures public accountability by investigating complaints against government agencies, promoting transparency through impartial oversight and protecting citizens' rights. The Auditor General enhances transparency by conducting independent financial audits, assessing public sector performance, and reporting on government spending efficiency. Both offices are key entities in upholding government accountability and fostering trust in public administration.

Reporting Structures and Processes

The Ombudsman typically reports to the legislature or a parliamentary committee, ensuring independent oversight of public administration and addressing citizen complaints, while the Auditor General reports directly to the legislature and focuses on financial audits and performance evaluations of government entities. Reporting processes for the Ombudsman involve investigation findings and recommendations submitted in annual or special reports aimed at improving administrative fairness, whereas the Auditor General delivers detailed audit reports assessing compliance, financial integrity, and efficiency typically accompanied by recommendations for corrective action. Both roles maintain transparency and accountability through timely, publicly accessible reports that facilitate legislative scrutiny and promote good governance.

Impact on Governance and Public Trust

The Ombudsman enhances governance by investigating complaints against public authorities, ensuring accountability and protecting citizens' rights, which strengthens public trust. The Auditor General improves governance through independent financial audits and performance evaluations of government operations, promoting transparency and responsible use of public funds. Together, these roles reinforce integrity in public administration and bolster confidence in government institutions.

Key Differences between Ombudsman and Auditor General

The Ombudsman primarily addresses complaints related to maladministration and protects citizens' rights by investigating grievances against government agencies, while the Auditor General focuses on auditing public accounts and ensuring transparent financial management within government operations. Unlike the Auditor General, who often conducts regular and systematic financial audits, the Ombudsman responds to specific cases and can recommend corrective actions without necessarily imposing financial penalties. Both roles serve as essential accountability mechanisms, but their functions differ in scope: the Auditor General enforces fiscal oversight, whereas the Ombudsman champions administrative fairness.

Conclusion: Choosing the Right Oversight Mechanism

Selecting the appropriate oversight mechanism depends on the specific objectives of accountability and transparency within government operations. The ombudsman specializes in addressing public grievances and ensuring administrative fairness, while the auditor general focuses on financial compliance and performance audits across government entities. Balancing these roles enhances comprehensive oversight, promoting both ethical governance and fiscal responsibility.

ombudsman vs auditor general Infographic